Loan with Collateral: Can You Keep the House If the Loan Unpaid?

By: Atty. Eugenio L. Riego II, LLB, MPA, REB

(Spoiler: No, You Can’t Just Grab the Title and Move In)

Let’s say we have a certain Pedro — not your average Pedro, but a Pedro with a solid bank account, a taste for imported coffee, and a penchant for lending money like a microfinance tycoon.

One lazy Sunday, Juan, an old friend who once copied Pedro’s homework in high school, showed up asking for a loan of PHP 100,000. Pedro, full of nostalgia (and caffeine), agreed.

To show he was serious, Juan gave Pedro the original title to his residential house and lot. No paperwork, no notary, just good old “mano-mano” (handshake deal) and Juan’s assurance:

“I promise to pay after one year.”

Moved by the gesture — and possibly the smell of old paper from the title — Pedro kept the document and waited.

Fast forward to ten years later…

While cleaning his office and sorting through papers (most of which were never filed with BIR), Pedro stumbled upon Juan’s title. Memories came flooding back.

“Ah yes, the unpaid loan!”

So, off he went to Juan’s house, eager to collect… or, in his words:

“reclaim what is rightfully mine.”

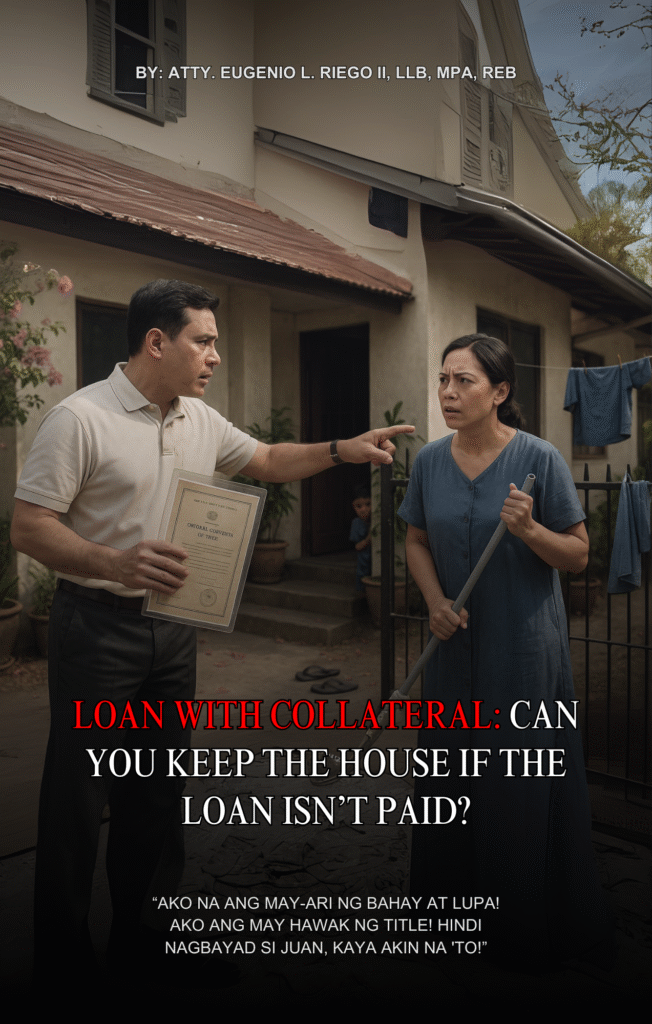

Unfortunately, Juan had passed away three years prior. Pedro then informed Juan’s family, in full legal drama:

“Ako na ang may-ari ng bahay at lupa! Ako ang may hawak ng title! Hindi nagbayad si Juan, kaya akin na ‘to!”

THE LEGAL ANSWER

Is Pedro now the owner of the property just because he holds the original title and Juan didn’t pay the loan?

Answer: Absolutely not.

Holding the title does not make you the owner, especially when the alleged transaction was undocumented, unnotarized, and involved no transfer of ownership through proper legal means.

In law, ownership over real property (land, house, etc.) does not transfer merely by non-payment of a loan, even if the borrower surrendered the original title. At best, Pedro was a creditor — not an instant property tycoon.

The remedy available to him was to file a proper case to recover the loan, and if granted, to have the property sold at public auction through foreclosure or attachment, not self-declared ownership.

In the absence of a public instrument, notarized deed, or a judicial foreclosure, Pedro cannot just waltz in with a title and claim ownership.

This is not Monopoly.

THE SUPREME COURT CASE

This situation is strikingly similar to the Supreme Court case:

Repuela, et al. v. Estate of Larawan, et al., G.R. No. 219638 (2016)

The case involves a dispute over a property in Cebu City, Philippines, originally owned by Lorenzo and Magdalena Repuela. After their passing, their children Marcelino and Cipriano Repuela succeeded as owners of the property.

The case revolves around a transaction in which the Repuela brothers allegedly signed over the property title to Otillo Larawan and his spouse. The Repuela brothers claimed that it was a mortgage to secure a loan, while Larawan’s family claimed it was a sale.

After a trial, the Regional Trial Court ruled in favor of the Repuela brothers, declaring the transaction as an equitable mortgage. However, the Court of Appeals reversed this decision, and the Supreme Court ultimately reinstated the ruling in favor of the Repuela brothers, considering the circumstances of the transaction, their continued possession of the property, and the presumption of mistake or fraud due to their lack of understanding.

This decision also outlined an interest rate for the Repuela brothers’ mortgage indebtedness.

The Court added that:

“A conveyance of land, accompanied by registration in the name of the transferee and the issuance of a new certificate, is no more secured from the operation of this equitable doctrine than the most informal conveyance that could be devised.

In an equitable mortgage, title to the property in issue, which has been transferred to the respondents actually remains or is transferred back to the petitioner as owner-mortgagor, conformably to the well-established doctrine that the mortgagee does not become the owner of the mortgaged property because the ownership remains with the mortgagor pursuant to Article 2088, of the Civil Code.”

Moral of the Story According to the Court?

Don’t confuse possession of paper with possession of property.

One fits in a folder; the other has a roof.

THE QUICK LEGAL ADVICE

So, dear readers, let this tale be your land lesson 101:

Titles are not like horcruxes — holding one doesn’t magically make you the master of the house and lot.

Just because someone gives you their title doesn’t mean you own their property. Otherwise, we’d all start accepting titles as “pasalubong” in every birthday party.

“Uy, title mo? Salamat ha, akin na ‘to!”

If you’re lending money and the other party offers land as collateral, please — for the love of law and sanity — put the agreement in writing, have it notarized, and execute a proper Real Estate Mortgage.

You know, do it the way our Civil Code imagined it should be, not like you’re bartering goats in the medieval period.

And if you’re the borrower?

Pay your loan.

Ghosting your lender might seem tempting, but it’ll come back — like an old title from a dusty drawer — and haunt your family ten years later.

In the end, Pedro should’ve called a lawyer instead of assuming he became a landowner by title osmosis.

Sadly, the law doesn’t work like YouTube tutorials —

you can’t “click ownership” by possession alone.

So, keep your titles safe, your contracts written, and your loans paid.

Or else, 10 years later, someone might show up at your doorstep with a title in hand, claiming:

“I am your new landlord, Exhibit A: your title.”

And your only reply will be:

“You can take the title… but not the house slippers.”

Read the latest blog – Will AI Replace Real Estate Agents What Professional Must Know

One Comment